Design & Strategy

I’m Victor J. Brunetti, a User Experience leader specializing in designing AI-driven products. My teams and I craft delightful experiences that make complex experiences beautifully clear.

Portfolio

-

![Cruise]()

Cruise

The Future of Autonomy, Today

-

![Google Store]()

Google Store

Brick and Mortar Revival

-

![Google Shopping Ads]()

Google Shopping Ads

Meeting Customers Where They Are

-

![Google Customer Conversations Platform]()

Google Customer Conversations Platform

AI-powered Contact Center of the Future

-

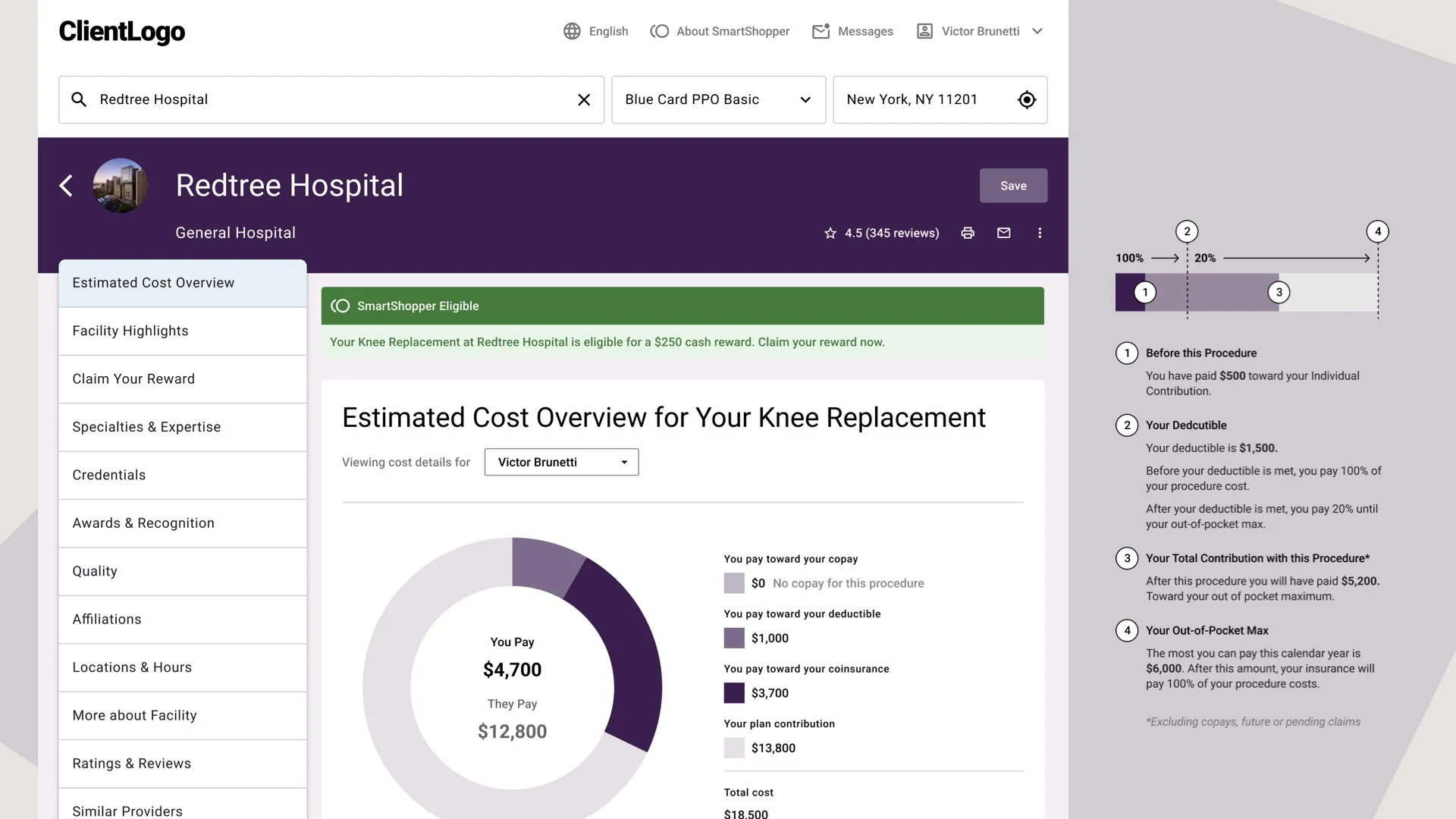

![Vitals]()

Vitals

Lowering Prices by Shopping for Healthcare

-

![McKinsey & Company]()

McKinsey & Company

Upping a Legacy Telco’s Game

-

![McKinsey & Company]()

McKinsey & Company

Increasing Pharma Efficacy with Digital

-

![Facebook]()

Facebook

Taking on Yelp at Facebook with Questions

-

![MedOS]()

MedOS

Mobile Operating System, Just for Doctors

-

![Gen Art]()

Generative Art

Generating Images with Flash ActionScript 2.0

Case Studies

-

![Tomorrow’s Autonomy, Today]()

Tomorrow’s Autonomy, Today

Let's get this out of the way upfront: Autonomous vehicles don’t exist. What we call "robot cars," "robotaxis," or "autopilot" is actually a combination of fully autonomous systems, partially autonomous systems, and Remote Assistants (tele-ops people). Today's vision of autonomy is delivered through a combination of an autonomous stack (onboard sensors + AI) and Remote Assistance.

-

![Contact Center of the Future]()

Contact Center of the Future

By 2018, Google’s supported product portfolio had grown exponentially compared to just 5 years prior, with no end in sight. Phones, watches, tablets and laptops, connected home devices, TV & media, Workspace, Ads, Search and Maps, etc. needed a human agent on standby if something went wrong. The cost of supporting these products with staffed contact centers risked exploding out of control.